I speak to many business owners that want to stay as a sole trader rather than register as a limited company. Most of these are making profits (before drawing money themselves) of more than, say £20,000 per year. When I ask them why this is, there are normally two responses:

- I don’t make enough to make it worthwhile

- I don’t want the hassle of running a limited company

I’ve addressed both of these points in this article, and then I’ve given the number 1 reason why you should be operating as a limited company rather than as a sole trader.

I don't make enough to make it worthwhile

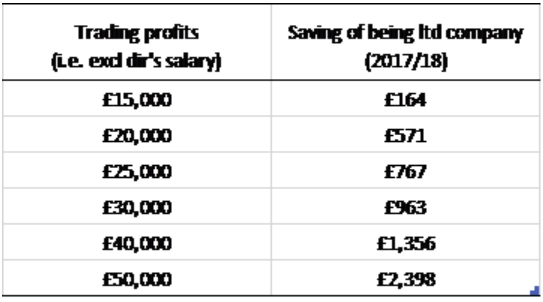

You’d be surprised by the low level of earnings which makes a limited company worthwhile.

The amounts in the table below are based on the 2017/18 tax year and are based on earnings before owner’s drawings[1].

You can see that even at low levels of profitability, being a limited company saves tax.

I don’t want the hassle of running a limited company

The difference between running a limited company and a sole trader isn’t as large as you might think.

In both sole traders and limited companies, you must keep business records, register for VAT where necessary, and submit returns to HMRC.

Under a limited company, you will need to submit annual accounts to Companies House, but any good accountant (and of course CFO360 UK!) will do this for you.

Most sole traders that I speak to have an accountant to do their tax returns anyway. And when they don’t, I always advise that they should (see this article on whether your small business needs an accountant). So even if the limited company accountant is a bit more expensive because of the (small) amount of additional work, the extra fees are more than covered by the tax saving shown in the table above.

The number 1 reason you should operate as a limited company

As a sole trader, when things go wrong, it is you, as the business owner who is affected.

So, for example, if someone gets injured and your business gets sued, it’s you as a person who is getting sued. You may then lose your house and any other assets you have. You may also go bankrupt if you don’t have enough assets to cover the payout. And this then affects your credit rating which reduces your chances of getting mortgages in the future.

Under a limited company, the very worst that can happen is that the company goes into liquidation and the assets that belong to the company are sold off to pay your debts. But unless you as a director have acted negligently or fraudulently, that’s as far as it goes. Your house is intact; your credit rating is intact.

And then when the limited company has been liquidated, you can set up a new one so that you can continue to earn an income.

When a sole trader is best

So, why are there so many sole traders? The main reason, I believe, is that the misconceptions addressed here are so common among business owners.

There are, however, times where being a sole trader is best:

- You’re making, and will continue to make profits (excluding drawings) of no more than £15,000 per year

- There is no, or negligible, risk of something going wrong in your business

- You have no plans to grow the business

- You do your sole trader accounts yourself and would prefer to continue to do that.

Final thoughts

For me, just the constant worry about the security of your house and credit rating that you have as a sole trader is enough to justify setting up a limited company.

But added to that are the tax savings and the fact that with an accountant like CFO360 UK, it’s no more hassle.

Most sole traders set up as such because of the misconceptions they have on the difficulties of operating as a limited company.

CFO360 UK work with small limited companies that are already set up, and those that haven’t yet registered as a limited company. We do all the registration of the company at no extra cost, and set you up to be a high growth and high profitability company. Give us a call to find out how, on 0203 950 3997 or email hello@cfo360.co.uk.

[1] Under a limited company, you don’t have drawings, but instead, get your income through a combination of salary and dividends. But don’t worry, CFO360 UK sort this all out for you.