Saving For School Fees? The Sooner You Start, The Better

There’s no getting away from it, children are expensive, especially if you are planning to send them to private school and/or university. But the sooner you start to put money away to save for these fees, the better, as it means you can put aside a smaller amount of money each month, and still watch it grow over time to meet your goals.

One of the best savings vehicles to help save for your child’s future is a Junior ISA (JISA), as the money inside this product will grow free of income tax and capital gains tax, which helps to maximise not just the money you put in, but any growth you see over the years.

You could also benefit from an increase of around 50% in the overall fund by the time your child reaches 18, providing you start early enough, according to recent research from Fidelity International. But no matter when you start, saving for your child’s future is a wise move.

Why should you use a Junior ISA?

Using a JISA is a sensible way to build a pot of money for your child, which can help to pay for various milestones such as university fees, a wedding, or even as a deposit to help them to buy their first home. Parents, grandparents, plus wider family and friends can all add money to the JISA, and the tax breaks explained above make it an appealing investment vehicle, and it will be in your child’s name.

You can open either a cash JISA or stocks and shares JISA for your child, and you can put up to £9,000 each year into JISAs for each child, as a maximum across both types. The money can be added to year after year, and will become available to your child when they reach 18.

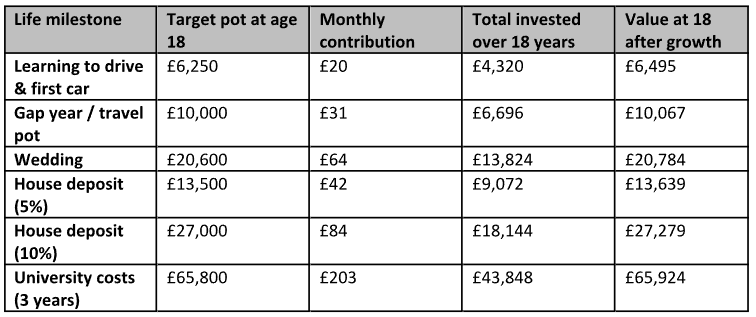

It will be very useful, because even at today’s prices, these milestones cost a lot of money. The table below gives some examples of how much various life events currently cost, and shows how much you would have needed to save over the last 18 years per month to meet these estimated costs. The values assume a 5% growth per year, less a 0.75% annual management charge, but don’t take inflation into account, which over time will erode your spending power as costs rise.

Source: Fidelity International

The importance of planning ahead

Most parents wouldn’t be able to save enough money to cover all their child’s life events, or even some of them, depending on their circumstances. But the figures in the table show how effective it is to start saving as soon as possible.

Jemma Slingo, Pensions and Investment Specialist, Fidelity International said: “For many families, the aim is simply to take some pressure off at key moments – whether that’s helping with first-year university costs, contributing towards a house deposit, or giving their child a financial cushion as they start adult life.

“What matters most is starting early, setting a contribution that feels manageable, and sticking with it.”

We can help you

If you are already saving for your children and want to check things are on track, or you would like to start, then please contact us and we will do everything we can to assist you.