Director’s loan account (DLA)

Introduction

We advise using a combination of the Director’s Loan Account (DLA) and dividends to ensure that you can take out money from the company in the most flexible way, whilst ensuring that any dividends declared are legal.

For a dividend to be legal, it needs to be made from ‘distributable profits’.

You also need dividends to be properly documented (which we’ll do for you), to reduce any risk that HMRC try to tax these amounts as if it was a salary, which would result in you paying more tax than necessary.

Director’s loan account (DLA)

Here’s the list of transactions that would go through your DLA. Next to each, we show whether it will be increasing (+) or decreasing (-) your DLA (i.e. whether the company owes you money for that transaction, or you owe the company money):

- Transferring money from you to the company: (+)

- Processing a dividend: (+)

- Processing a salary (we do that for you): (+)

- Paying for business items from a personal account: (+)

- Transferring money from the company to you: (-)

- Paying for personal items from a business account: (-)

As an example, let’s say that CFO360 UK processes a salary of £758 for you. This will increase the amount that the company owes you. Then, if you withdraw that salary of £758 from the company, that will decrease the amount that the company owes you: both transactions will go through the DLA, summing to zero.

What you should watch out for

There are two main things you have to watch out for, as both items will end up costing you more in tax, but both can be easily managed:

- DLA owing by you to the company (showing as a negative on your balance sheet) of more than £10,000

- DLA owing by you to the company at year end that isn’t repaid through either salary or a dividend within 9 months following your year end.

To manage both of these, you simply need to ensure that you are declaring dividends so that any amounts that you’ve taken out of the company are matched by those dividends (less any salary you’ve taken).

We suggest you process a dividend either every month, or every quarter, depending on how much money you’re taking from the company. This is to:

- Prevent you from paying additional tax because of one of the two points shown above.

- Enable you to review your distributable profits before declaring a dividend (see ‘Distributable profits’ section below)

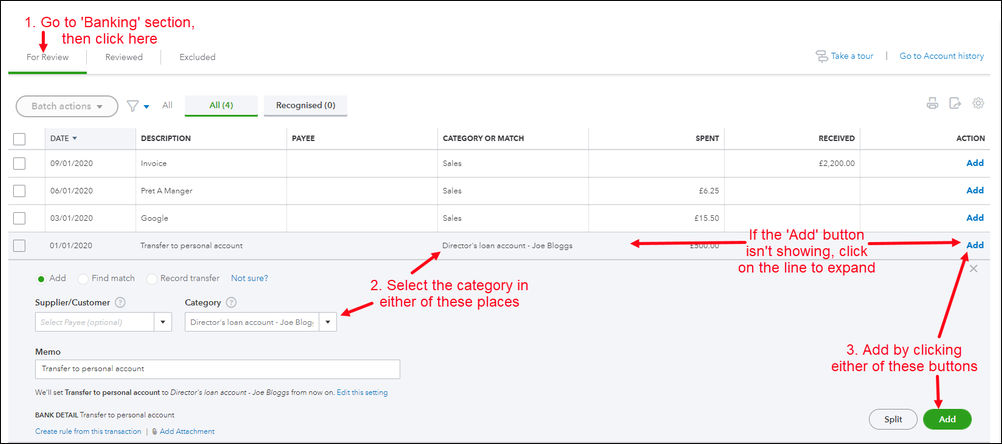

How to record in QBO

When you transfer money from your business account to your personal, you’ll see the transaction on your bank feed.

- Go to ‘Banking’, and find transaction in the ‘For review’ tab

- Select category of ‘Director’s loan account’

- Add the transaction to the books