Company Size Thresholds To Increase In The UK From April

The official classification of company sizes is set to change from April, with many firms being identified as smaller than they were previously, which should make filing company accounts more straightforward.

The new legislation, The Companies (Accounts and Reports) (Amendment and Transitional Provision) Regulations 2024, will increase the thresholds at which micro, small, and medium-sized companies are classified, which aims to cut the complexity in financial reporting. The existing thresholds have not changed since 2013, so it is also designed to take inflation into account in the intervening period.

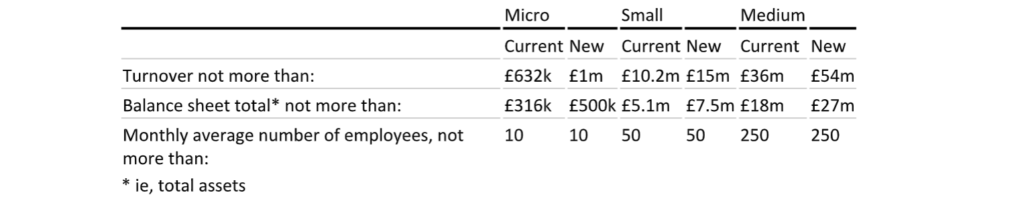

The new thresholds, which come into effect on April 6, will determine the size of a business for a fiscal year, if two of three criteria are met:

Source: ICAEW

These new thresholds will apply to limited liability partnerships (LLPs) as well as limited companies.

What is the impact of these changes?

Government estimates suggest as many as 113,000 companies and LLPs that have previously been categorised as small will become micro entities. A further 14,000 are expected to move from medium-sized to small companies, and 6,000 from large to medium-sized. Any company that can go down a category will see a lower burden in reporting and auditing requirements.

Companies moving from the medium-sized to small category will no longer need a statutory audit of their accounts, or to provide a strategic report. They will also have simpler accounting requirements. But these changes would depend on whether they are part of a group. Any company moving from a small to micro entity will no longer have to provide a Directors’ Report.

What benefits will larger companies have?

Companies recategorised as medium-sized rather than large will be exempt from some Strategic Reporting requirements, including a Section 172(1) statement which outlines how directors of the company have taken stakeholder and other interests into account as per section 172, CA 2006 for

the financial year.

Fahad Asgar, Technical Manager, Corporate Reporting Faculty, ICAEW, said: “The legislation includes a transitional provision for the application of the ‘two-year consecutive rule’. When determining company size for a financial year beginning on or after 6 April 2025, the transitional provision allows preparers to assume that the new thresholds had been applicable in the previous financial year. This look back is only available for the application of the two-year rule. As a result, companies and LLPs can benefit from the threshold uplift as soon as possible after the legislation comes into effect.

“Ensuring proportionality and removing duplicative reporting requirements is an important first step towards a modernised model for UK corporate reporting.”

Large and medium-sized entities will also see a raft of requirements that have previously been necessary for their Directors’ Report removed. So, they will no longer have to include information on:

- Financial instruments.

- Important events that have occurred since the end of the financial year.

- Likely future developments.

- Research and development.

- Branches outside the UK.

- The employment of disabled people (this requirement is also being removed for small entities).

- Engagement with employees.

- Engagement with customers and suppliers.

Source: ICAEW

You can find more information outlined in the Government’s explanatory memorandum.

We can help you meet your obligations

If you are unclear about what these changes will mean for your business, then please get in touch and we would be happy to give you the guidance you need.